When business owners think about risk, the usual concerns come to mind: severe weather, lawsuits, cyber threats, supply chain disruptions. Those risks are visible and easy to name.

There’s another risk that’s easier to miss. Changes in commercial property insurance in Maryland are being driven by inflation and rising property valuations, which have increased the cost of repairing or rebuilding property.

In many cases, this shift has created coverage gaps that aren’t apparent until after a loss.

Below, we break down how these gaps develop, why they matter, and how businesses can address them before a loss forces the issue.

How Rising Property Values in Maryland Are Creating Insurance Coverage Gaps

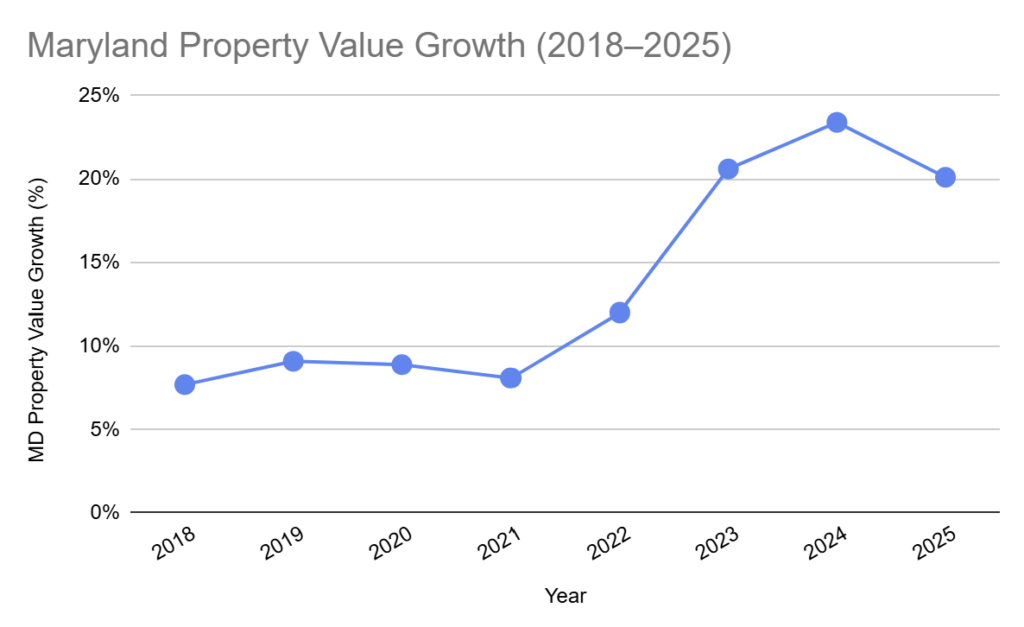

Maryland Department of Assessments and Taxation data shows that property values across the state have risen decisively.

Between 2023 and January 1, 2026, Maryland assessed 789,178 residential and commercial properties statewide. During that period, 87.14% of those properties increased in value.

Property values jumped in 2023 and rose by 20.1% in 2025.

Data Source: Maryland Department of Assessments and Taxation, January 1, 2026 Assessment Report

When property values increase this much, it’s a signal that the cost to repair or rebuild has changed.

The Impact of Inflation on Construction Costs

Outside of unusually high inflation years like 2021 and 2022, non-residential construction costs have increased by about 3.8% per year since 2011. That long-term trend reflects normal increases in labor, materials, and regulatory requirements.

In 2025, inflation pushed construction costs above that historical pace. Labor shortages, higher material prices, and longer permitting timelines all contributed to cost increases estimated at 4.0–4.4%.

Property Value & Inflation Impact on Business Insurance

Rebuild costs in Maryland in 2026 are significantly higher than many business insurance policies were designed to account for.

Typically, property insurance limits are based on estimated rebuild costs at the time a policy is written or last reviewed. When property values and construction costs accelerate, those estimates can quickly fall out of sync with current conditions.

If your limits haven’t changed since 2023, you may be exposed to coverage gaps you’re not aware of. Your limits likely no longer reflect today’s repair or rebuild costs after a loss.

The 2026 Insurance Coverage Gaps Most Businesses Don’t See

Coverage gaps don’t usually come from inattention. They develop when policies are built on assumptions that no longer reflect current conditions.

Commercial property insurance policies written before or during 2023—when property values in Maryland spiked—often assumed lower labor costs, lower material pricing, and shorter rebuild timelines than what businesses face in 2026.

When policy limits are still based on older estimates, coverage can fall short even if nothing else has changed, resulting in:

1. Underinsured Buildings

The insurance limit on the building may be lower than what it would cost to repair or rebuild today. After a loss, coverage may not be sufficient to fully restore the property.

2. Coinsurance Penalty Explained

Many property policies require the building to be insured to a certain percentage of its replacement value.

If the limit is too low, the insurer may reduce the claim payment—even for partial losses—leaving the business to cover more of the cost out of pocket.

3. Delayed or Incomplete Rebuilds After a Loss

Rebuilding can stall when policy limits don’t align with the actual costs of rebuilding. Businesses may need to delay repairs, rebuild only part of a facility, or make compromises to get back up and running, which can extend downtime and disrupt operations.

What’s worse, these gaps often aren’t visible until a claim occurs, when replacement costs are measured against limits that no longer reflect today’s reality.

How You Can Stay Ahead of Coverage Gaps in Your Commercial Property Insurance

Rather than waiting for a loss to reveal gaps, you can take a more proactive approach to your property coverage in 2026 by doing the following:

1. Revisit Replacement Cost Assumptions

Start by revisiting replacement cost assumptions, not just overall policy limits. Look closely at what it would actually cost to repair or rebuild today, based on current labor rates, material pricing, and permitting conditions.

2. Stress-Test Policies Against Current Construction Costs

By comparing current limits to realistic rebuild scenarios, you can identify where coverage may no longer align with present-day conditions before a claim occurs.

3. Make Coverage Adjustments Before a Loss

When gaps are identified, updating coverage during a renewal or mid-term review allows you to address them on your terms. Being proactive with adjustments is far more manageable than trying to resolve coverage issues after a loss has already occurred.

All of this can feel overwhelming—especially when inflation, construction costs, and insurance terms are changing at the same time, but you don’t have to figure it out alone.

Why Working With a Local Maryland Broker Matters More Than Ever

Property values and construction costs in Maryland have changed quickly over the last few years, which directly affects how property insurance responds after a loss. Coverage decisions now depend less on standard assumptions and more on what rebuilding costs are in local markets.

At Gerety Insurance, we focus on how changes in Maryland property values and rising costs affect insurance coverage. We help clients review replacement values, coinsurance requirements, and policy limits so coverage reflects current conditions in Maryland—not outdated, general assumptions.

If you’re unsure whether your current coverage still reflects today’s rebuild costs, a commercial insurance review is a good place to start.

Request a quote to begin the conversation. We’re here to help protect your business by making sure your coverage works as intended when you need it.