If your insurance rates have increased recently—and you’re struggling to understand why—you’re not alone. Many Maryland drivers and homeowners are opening renewal notices with higher premiums, fewer discounts, and more questions than answers.

What’s happening isn’t personal, and it isn’t the result of a single decision or mistake. The insurance market itself has changed. Carriers across the country are adjusting how they price risk, how selective they are about who they insure, and what types of policies they’re willing to write.

The industry calls this a “hard” insurance market.

Below, we break down what that means, how it affects auto and home insurance in Maryland, and what you can do to confidently navigate your options and find savings, even in a challenging market.

What is a “Hard” Insurance Market?

A hard market is an “upswing in the insurance market lifecycle” when insurance carriers tighten up.

They raise rates, become more selective about who they insure, reduce discounts, and sometimes stop writing certain types of policies altogether.

This shift happens when the insurance business becomes less profitable overall—not because of individual policyholders, but because of broader financial pressures on insurers.

Our current hard market is driven by a few clear factors:

- Claims are more expensive and more frequent. Higher repair costs, medical expenses, labor, and parts mean even routine claims cost significantly more than they did in the past.

- Insurers are earning less on investments. With reduced returns, insurers rely more heavily on premiums to cover losses.

- Pricing is catching up to reality. For years, rates didn’t keep pace with rising costs, and carriers are now correcting for that gap.

- Insurers are limiting exposure. Fewer policies, tighter underwriting, and less pricing flexibility are part of how carriers manage risk in this environment.

In a soft market, insurers compete aggressively for business. In a hard market, they protect their bottom line first.

As a result, even responsible drivers and homeowners—people with no recent claims and long policy histories—are seeing increases. It’s why rates can change even when nothing about you has.

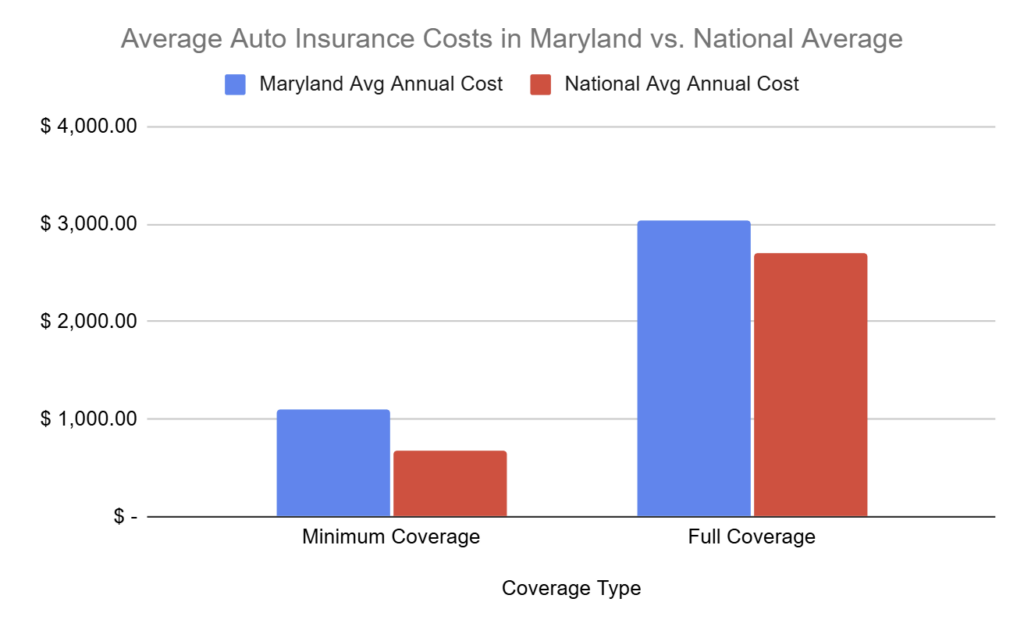

Why Auto Insurance Got Hit First (and Hardest) in Maryland

Maryland drivers don’t start on level ground when it comes to auto insurance pricing. With premiums already above national averages, market-wide increases tend to hit harder here.

The following figures are based on industry data from November 2025.

Source: Bankrate analysis of data from Quadrant Information Services.

Maryland’s higher averages reflect a mix of higher claim costs, greater legal standards, and market dynamics that affect overall auto insurance prices.

For instance,

1. Maryland has a relatively high number of uninsured drivers.

When uninsured drivers cause accidents and can’t pay for damages, insured drivers ultimately absorb those costs through higher premiums.

That’s why uninsured motorist coverage is especially important in Maryland, and one reason rates continue to rise even for drivers who never file a claim.

If a driver is even 1% at fault in an accident, they may be unable to recover damages from the other party. Consequently, no-fault coverages like Personal Injury Protection (PIP) play a larger role here than in many other states.

These coverage structures affect claim frequency and insurer payouts, contributing to overall pricing pressure.

3. Auto repairs are significantly more expensive than they used to be.

Modern vehicles rely on advanced technology, sensors, and safety features that make even minor accidents more costly to fix than in years past.

As repair and parts costs rise, insurers pay more per claim, which puts upward pressure on premiums for all Maryland drivers.

Why “Good Drivers” Still See Increases in Maryland

Many Maryland drivers are seeing higher premiums despite clean records and no recent claims. In this hard market, pricing is driven less by individual behavior and more by how insurers assess risk statewide.

Even when a driver’s profile hasn’t changed, market conditions can outweigh personal history. That’s why comparing options and reviewing coverage regularly matters more now than it did in the past.

Before we talk about how to compare policies and find savings, let’s take a quick look at what’s happening with homeowners insurance.

What’s Happening with Home Insurance in Maryland?

Homeowners insurance in Maryland is affected by the same hard-market forces as auto, but the story here is more measured.

Yes, Rates Are Rising

Homeowners insurance premiums in Maryland are increasing, largely due to higher rebuilding costs. Inflation, labor shortages, and rising material prices have made it more expensive to repair or rebuild homes than it was just a few years ago.

These pressures have pushed replacement costs higher, which in turn affects how policies are priced and how much coverage homeowners need.

No, Maryland Isn’t Florida or California

It’s important to keep this in perspective. Maryland is not experiencing the kind of homeowners insurance disruption seen in high-risk states like Florida or California.

Historically, Maryland homeowners have paid below the national average for homeowners insurance, and costs here have remained relatively stable compared to other Mid-Atlantic states. There hasn’t been widespread carrier withdrawal or extreme premium volatility tied to catastrophic weather risk.

That said, homeowners insurance costs are rising—and are likely to continue rising—as higher rebuild costs push replacement values upward.

Why Rebuild Costs Are Driving Home Insurance Changes in Maryland

From 2023 to 2025, property values in Maryland increased by 20.1%, raising the amount insurers would need to pay to rebuild homes at today’s prices. At the same time, construction costs have continued to rise due to higher labor, material, and regulatory expenses.

These higher rebuild costs increase the size of potential claims, which insurers account for when setting coverage limits and pricing. In a hard market, that adjustment happens more deliberately on the homeowners side, reflecting higher replacement values rather than sudden shifts in risk.

As a result, homeowners insurance in Maryland is seeing upward pressure, but in a more measured, predictable way than auto insurance.

Why Shopping the Market Matters More Than Ever

Insurance pricing is less consistent and less predictable than it used to be. The carrier that was competitive last year may not be the best option today, and in some cases, may no longer be the right fit at all.

In today’s hard market, remember…

One carrier is not the market.

Rates, underwriting rules, and coverage options vary widely from one insurer to another. Comparing a single carrier’s renewal to last year’s price doesn’t show how the broader market has changed, or whether better options exist elsewhere.

Carrier appetite changes constantly.

Insurance companies regularly adjust what types of risk they’re willing to take on. A carrier that aggressively pursued business last year may tighten underwriting or raise rates this year, while another steps in with more competitive pricing. And oftentimes, these shifts happen behind the scenes and often without notice to consumers.

So, what can you do?

You can review your renewal, request quotes, and try to compare options on your own. But in a hard market, market dynamics change quickly and aren’t easy to track without industry context.

Another option is working with an independent insurance agency.

How an Independent Agency Helps in a Hard Market

If you want help evaluating your insurance options, it’s important to understand that who you work with determines how many options you can actually compare.

For instance, direct writers represent a single insurance company, which means their recommendations are tied to that company’s products and pricing. This restriction limits your ability to compare and evaluate different options across the market.

At Gerety Insurance, we’re an independent agency, meaning we’re not tied to one carrier.

We work with multiple insurance companies and help our clients compare options across the market.

Having this flexibility is especially important in a hard market. Different carriers respond to market pressure in different ways—some tighten guidelines, others adjust pricing, and some remain more competitive for certain types of risk.

Our role is to understand those differences and help evaluate which options make sense based on your specific situation.

How We Help Our Clients Find Savings in a Hard Market

For us, finding savings in a hard market doesn’t mean choosing the cheapest option available. We take a practical approach to identifying savings while maintaining appropriate coverage.

Here are some of the ways we do so:

1. Re-Shopping Auto When It Makes Sense

Auto insurance is often the most volatile line in a hard market. When pricing or guidelines shift, we re-shop policies across our carrier partners to see how different insurers are responding to similar risks.

Sometimes that leads to meaningful savings; other times, it confirms that staying put is the better option.

2. Adjusting Structure, Not Just Price

Savings don’t always come from switching carriers. In many cases, we look at how a policy is structured: coverage limits, deductibles, endorsements, and how different pieces work together. Small structural adjustments can improve value without reducing protection.

3. Bundling Intentionally

Bundling can be effective, but only when it makes sense for the overall risk profile. We evaluate when bundling actually improves pricing or coverage and when separating policies is the better long-term choice.

4. Knowing When Not to Move a Policy

In a hard market, switching isn’t always the answer. Some carriers remain competitive for certain risks, and moving a policy at the wrong time can introduce higher costs or reduced coverage. Part of our role is recognizing when holding steady is the smartest decision.

Finding savings isn’t a one-time exercise or a reaction to a single renewal. Market conditions continue to change, and decisions that make sense today may need to be revisited as carrier appetite, pricing, and coverage requirements evolve.

Our role is to provide ongoing guidance that helps our clients navigate those shifts over time, weighing trade-offs and adjusting strategies thoughtfully as the market moves.

Navigating a Hard Market With the Right Partner

A hard market can feel discouraging, but it doesn’t mean you’re out of options. With the right guidance, you can still make confident decisions that protect what matters, without overpaying or creating gaps in coverage.

At Gerety Insurance, we focus on helping clients feel confident in their coverage—even when the market is uncertain.

For more than 25 years, we’ve served Maryland families and businesses by putting people before policies. We provide clear guidance, proactive reviews, and ongoing support, so you don’t have to track carrier changes, decipher fine print, or advocate on your own.

If you’d like help reviewing your coverage or exploring your options, we’re ready to listen. Request a quote to start a conversation and gain a partner who’s looking out for you, not just your policy.